Abstract

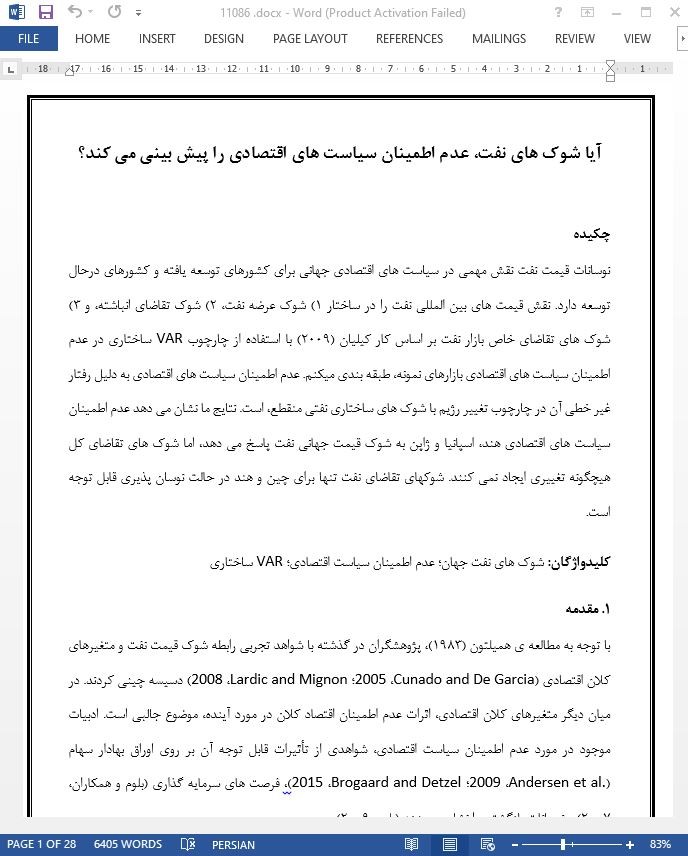

Oil price fluctuations have influential role in global economic policies for developed as well as emerging countries. I investigate the role of international oil prices disintegrated into structural (i) oil supply shock, (ii) aggregate demand shock and (iii) oil market specific demand shocks, based on the work of Kilian (2009) using structural VAR framework on economic policies uncertainty of sampled markets. Economic policy uncertainty, due to its non-linear behavior is modeled in a regime switching framework with disintegrated structural oil shocks. Our results highlight that Indian, Spain and Japanese economic policy uncertainty responds to the global oil price shocks, however aggregate demand shocks fail to induce any change. Oil specific demand shocks are significant only for China and India in high volatility state.

1. Introduction

Since the work by Hamilton (1983), researchers in the past are intrigued by empirical evidences of the relationship between oil price shocks and macro-economic variables (Cunado and De Garcia, 2005; Lardic and Mignon, 2008). Among other macro-economic variables, effects of macro-economic uncertainty about the future sparks great interest. Existing literature on economic policy uncertainty provides evidence of its significant effects on equity portfolios (Andersen et al., 2009; Brogaard and Detzel, 2015), investment opportunities (Bloom et al., 2007) and returns volatility (Bloom, 2009).

6. Conclusion

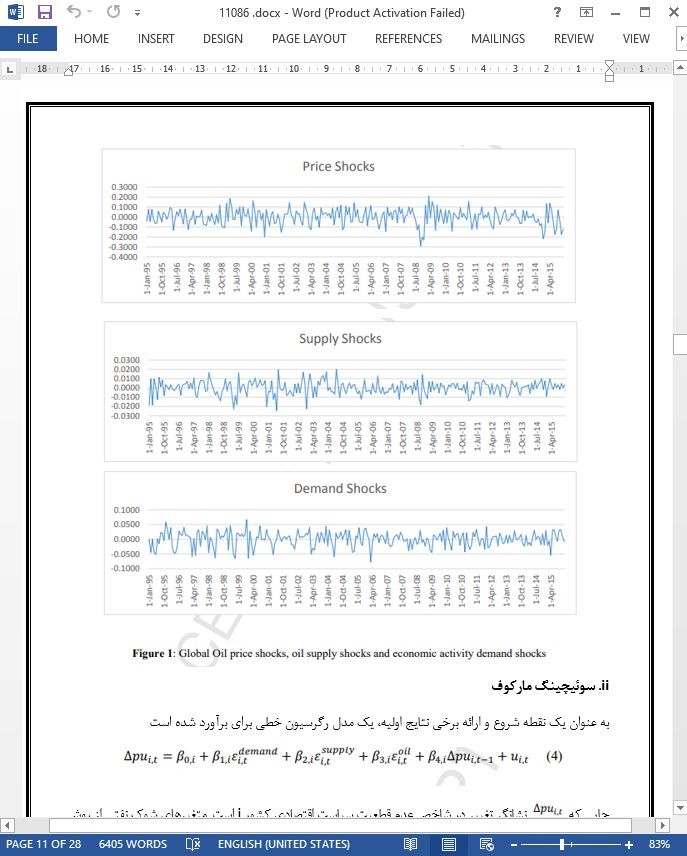

Current literature provides valuable insights about the impact of raising oil prices on different macro-economic variables. This is because of the importance of global oil prices in affecting any economy and an ever-increasing energy demand regardless of the economic status of any country. Any escalation in oil prices can induce either economic or macroeconomic policy uncertainty of a country. Although current strand of literature deals with the behavior of different economies to oil price fluctuations, author aims at capturing nonlinear behavior of oil using Markov regime switching model. This technique has the advantage of capturing non-linear behavior of oil prices that would be difficult to gauge with traditional non-linear models. To have a complete understanding of oil prices behavior on economic policy uncertainty, I introduced oil supply shock, aggregate demand shock and oil specific demand shocks. The effect of these shocks is captured by two regime states corresponding to low and high volatility state.