.svg)

.svg)

.svg)

ترجمه مقاله تاثیر شوک های داخلی و خارجی بر درآمدهای حاصل از تنوع بخشی پورتفولیو - نشریه MDPI

عنوان فارسی

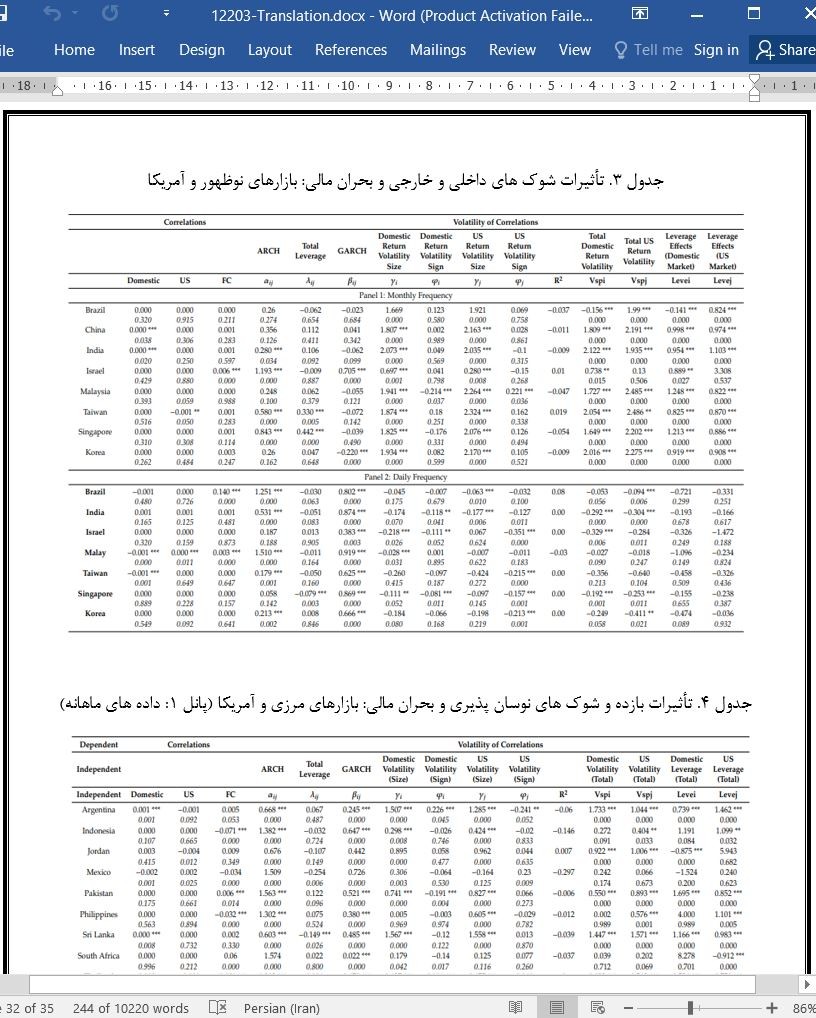

تأثیر شوک های داخلی و خارجی بر درآمدهای حاصل از تنوع بخشی پورتفولیو (سبد) و ریسک های همراه با آن

عنوان انگلیسی

The Influence of Domestic and Foreign Shocks on Portfolio Diversification Gains and the Associated Risks

صفحات مقاله فارسی

35

صفحات مقاله انگلیسی

26

سال انتشار

2019

رفرنس

دارای رفرنس در داخل متن و انتهای مقاله

نشریه

MDPI

فرمت مقاله انگلیسی

pdf و ورد تایپ شده با قابلیت ویرایش

فرمت ترجمه مقاله

pdf و ورد تایپ شده با قابلیت ویرایش

فونت ترجمه مقاله

بی نازنین

سایز ترجمه مقاله

14

نوع مقاله

ISI

نوع ارائه مقاله

ژورنال

شناسه ISSN مجله

1911-8074

کد محصول

12203

وضعیت ترجمه عناوین تصاویر و جداول

ترجمه شده است ✓

وضعیت ترجمه متون داخل تصاویر و جداول

ترجمه نشده است ☓

وضعیت ترجمه منابع داخل متن

ترجمه شده است ✓

وضعیت فرمولها و محاسبات در فایل ترجمه

به صورت عکس، درج شده است ✓

ضمیمه

ندارد ☓

بیس

نیست ☓

مدل مفهومی

ندارد ☓

پرسشنامه

ندارد ☓

متغیر

ندارد ☓

فرضیه

ندارد ☓

رفرنس در ترجمه

در داخل متن و انتهای مقاله درج شده است

رشته و گرایش های مرتبط با این مقاله

مدیریت، اقتصاد، حسابداری، مهندسی مالی و ریسک، مدیریت مالی، حسابداری مالی و اقتصاد مالی

دانشگاه

دانشکده اقتصاد، امور مالی و بازاریابی، دانشگاه RMIT، ملبورن، استرالیا

کلمات کلیدی

شوک های بازده، شوک های نوسان پذیری، بازارهای مرزی، بازارهای نوظهور، بازارهای توسعه یافته، همبستگی ها، همبستگی های نامتقارن

کلمات کلیدی انگلیسی

return shocks - volatility shocks - frontier markets - emerging markets - developed markets - correlations - asymmetric correlations

doi یا شناسه دیجیتال

https://doi.org/10.3390/jrfm12040160

۰.۰

(هنوز امتیازی ثبت نشده است)